"Recent data has already indicated strong growth in demand for spot yuan, which is evidence of the growing liquidity in the offshore yuan market, the increasing confidence of investors to trade in it and the growing diversity and sophistication of the offshore market," Boleat says.

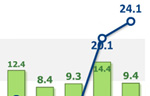

Spot yuan foreign exchange trading in London is estimated to account for 26 percent of the global offshore yuan spot market, according to City of London's statistics.

Last year, the London yuan offshore market made further development in terms of products and business scale, especially in foreign exchange trading businesses.

According to data released by the City of London, by the end of 2012, London achieved robust growth in trade-related yuan businesses. The volume of import and export financing increased by 100 percent, compared with the end of 2011, to 33.6 billion yuan.

London also saw a few yuan bond issues in 2012, including ones by HSBC and China Construction Bank.

China Construction Bank, the country's second-largest lender, launched a 1 billion-yuan London-listed bond, or a so-called dim-sum bond, in November 2012, the first Chinese borrower to issue bonds in the London yuan bond market.

"China Construction Bank's decision to float the bond in London is proof of London's growing stature as the Western hub for renminbi business," Osborne says.

Another example of a product that helped boost London's yuan liquidity is the repo transaction between UBS AG in London and HSBC Holdings Plc's Hong Kong branch, carried out in December 2012, with the Hong Kong Monetary Authority managing the collateral.

The deal allows HSBC to lend its yuan in Hong Kong to UBS in London, where the liquidity for yuan is smaller, so effectively helping London to deal with the risk of fragmented liquidity in London, says Candy Ho, HSBC's head of yuan business development in Hong Kong.

"Hong Kong has the most liquidity for renminbi, but there have also been a lot of renminbi transactions coming through different parts of the world," she says.

"By reducing the risk of fragmented liquidity and allowing funds to flow between different renminbi centers, overall offshore liquidity for renminbi will increase."

As London is not currently an offshore center for yuan, offshore yuan accumulated in London can only flow into the Chinese mainland via Hong Kong's clearing bank, Bank of China's Hong Kong branch. This allows European banks with yuan accounts to participate in the yuan Real Time Gross Settlement system in Hong Kong.

But Boleat says he does not see an urgent need for London to have a clearing bank because the Hong Kong arrangements serve London's needs.

Models at Ford pavilion at Chengdu Motor Show

Models at Ford pavilion at Chengdu Motor Show

Brilliant future expected for Chinese cinema: interview

Brilliant future expected for Chinese cinema: interview

Chang'an launches Eado XT at Chengdu Motor Show

Chang'an launches Eado XT at Chengdu Motor Show

Hainan Airlines makes maiden flight to Chicago

Hainan Airlines makes maiden flight to Chicago

Highlights of 2013 Chengdu Motor Show

Highlights of 2013 Chengdu Motor Show

New Mercedes E-Class China debut at Chengdu Motor Show

New Mercedes E-Class China debut at Chengdu Motor Show

'Jurassic Park 3D' remains atop Chinese box office

'Jurassic Park 3D' remains atop Chinese box office

Beauty reveals secrets of fashion consultant

Beauty reveals secrets of fashion consultant

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()