HONG KONG - China's financial system is more "robust" than widely thought and the recent cash crunch does not signal any systemic risk, according to a senior investment executive of one of the largest asset managers in the Chinese mainland.

Until Beijing pledged last week to ensure adequate funding, borrowing costs in the mainland spiked to record highs and stocks tanked, raising fears of a banking crisis that could compare with the 2008 one in the United States.

"In a few months time, people are going to look back on this and realize it's all noise," said Andrew Tan, chief investment officer at Hong Kong-based Harvest Global Investment, the international arm of Harvest Fund Management. The mainland-based parent manages more than $50 billion across asset classes in Asia.

Echoing Beijing's position, Tan said the tight cash market is the result of the People's Bank of China (PBOC) seeking to limit funds to a vast informal loan market as it works to shore up growth in the world's second-largest economy.

"We are saying loud and clear that we don't think there's a systemic risk in the Chinese financial system," Tan added. "The overall structure is much more robust than what most foreigners think."

But Harvest Global Investment has been underweight on Chinese financials. According to its fact sheet, at the end of May, the two top holdings in its China Equity Fund were Industrial and Commercial Bank of China (ICBC) and China Construction Bank (CCB).

Still, Chinese financials accounted for a combined 32.25 percent of the portfolio, compared to 40.5 percent weight on the MSCI China benchmark.

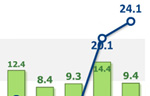

Through the end of May, this fund had outperformed in 2013, rising 3.7 percent compared with a 4.6 percent slide for the MSCI China. Between its inception in March 2012 and May 31, the China Equity Fund outshined the benchmark by rising 13.9 percent to 2.8 percent.

Some sectors eschewed

Harvest Global is playing the structural growth shift in China. It is eschewing sectors that benefitted from its old growth model, as coal and coal-based utilities, and embracing ones in which it feels China is moving up the value chain.

"We like Chinese companies that innovate," Tan said, adding that these companies also tended to be high precision industries in the medical and information technology sectors.

These sectors are also less susceptible to policy headwinds as Beijing moves the focus from low to high quality growth, Tan said. While he also favours the white goods sector, it does not figure in the fund's top 10 holdings.

Harvest Global counts Winteam Pharmaceutical, Sino Biopharmaceutical and TCL Communication Technology as among top 10 holdings in its China Equity Fund as of May 31.

"One trend is very clear: Chinese medical device makers are gaining market share on foreign companies from Germany and the US," Tan said. "At the same time, they are much more competitive in terms of their pricing and access to market."

In a change since the start of the year, Harvest Global managers have also cut coal producers and coal-based utilities from their portfolio with combating pollution a key focus for the new Chinese leadership.

Models at Ford pavilion at Chengdu Motor Show

Models at Ford pavilion at Chengdu Motor Show

Brilliant future expected for Chinese cinema: interview

Brilliant future expected for Chinese cinema: interview

Chang'an launches Eado XT at Chengdu Motor Show

Chang'an launches Eado XT at Chengdu Motor Show

Hainan Airlines makes maiden flight to Chicago

Hainan Airlines makes maiden flight to Chicago

Highlights of 2013 Chengdu Motor Show

Highlights of 2013 Chengdu Motor Show

New Mercedes E-Class China debut at Chengdu Motor Show

New Mercedes E-Class China debut at Chengdu Motor Show

'Jurassic Park 3D' remains atop Chinese box office

'Jurassic Park 3D' remains atop Chinese box office

Beauty reveals secrets of fashion consultant

Beauty reveals secrets of fashion consultant

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()