For global investors holding gold, the past few weeks must have been a happy time. Since the United States Federal Reserve announced a new round of "open ended" quantitative easing, or QE3, on Sept 13, gold prices have risen from $1,730 to $1,775 per ounce.

On Oct 2, Deutsche Bank even raised its 2013 gold price outlook to $2,113 per ounce, claiming in a research note that, "a surge in the gold price above this level ($2,000 per ounce) is only a matter of time".

Should this grab the attention of China?

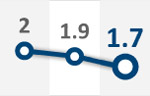

Its gold storage of 33.9 million ounces, although the fifth largest in the world, accounts for only 1.7 percent of its $3.3 trillion foreign reserves, much lower than the 75.4 percent of the US and 72.3 percent of Germany. So should China buy more gold?

Not necessarily, say Campbell R. Harvey, a professor at Duke University's Fuqua School of Business, and Claude B. Erb, managing director at First Chicago NBD Investment Management Company. In their opinion, "as long as China follows sound economic policies", there is no compelling necessity for it to buy gold.

In their newly released research paper, The Golden Dilemma, Harvey and Erb have analyzed what they call "the myths of gold", namely that it is regarded as a hedge against inflation and an alternative to low-return assets, and they discuss whether central banks in emerging markets should increase their gold stocks.

According to their research, gold as an honest currency can be a hedge against inflation, but it is more effective in the long term rather than the short term. Besides, as an honest currency, gold is more effective against hyperinflation, in which situation the public loses most, if not all, confidence in bank notes.

That is not the situation today, say Harvey and Erb, as the impact of QE3 will probably be similar to the impact of QE1 and QE2, both of which aroused worries though not noticeable worldwide inflation. As QE3 is to be implemented in almost the same way as the previous two rounds of quantitative easing, they believe it "a good bet" that QE3 would not result in higher inflation in the short term although the price of gold will rise.

But what about the long run?

In an e-mail interview with China Daily, Harvey gave two long-term reasons to consider owning gold: For an individual or company, distrust of his or her own government to maintain a sound currency; for a country, inadequate faith in the value of the currency with which its trading partners buy its exports.

In the case of China, Harvey said "its historically low level of gold reserves made sense for a rapidly growing country that had faith in the way that its trading partners managed their economic affairs". Of course, given the economic malaise in the United States and Europe, China has every reason to question its faith in the value of the dollar and the euro. But buying gold is not the only option. It can take other measures and diversify its foreign reserves.

Actually, it is hard to find any connection between the size of a country's gold reserves and the health of that country's economy. Harvey cited the examples of the US and Germany, who despite their large gold reserves still suffered from periods of high inflation and exchange rate volatility.

Harvey concluded, the key to maintaining a healthy economy is sound economic policies, and there was no need for China to increase its gold reserves.

"Gold might be a barometer of failed economic policies. Investing in barometers is not the answer; responsible economic policies are."

The author is a journalist with China Daily.

E-mail: zhangzhouxiang@chinadaily.com.cn

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()