Structural problems within industries, not adverse external factors, are responsible for China's economic slowdown

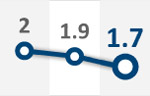

China's 7.8 percent economic growth in the first half of this year is enough to overshadow the rest of the world, but it has still raised concerns among some people - used to China's fast-paced growth - over the gloomy prospect of the world's second largest economy.

The 7.6 percent GDP growth in the second quarter is not only lower than the already decelerated first-quarterly 8.1 percent, but also the first time that China's GDP has fallen below 8 percent in nearly three years.

Before a judgment is passed over China's macroeconomic data in the first half of this year, at least two questions should be answered. First, is the 7.8 percent economic growth a short-term economic slowdown or has China's economic momentum really reached a turning point? Second, is China's economic downturn caused by external factors such as the sovereign debt crisis in Europe or is it the result of the country's long-term deep-rooted economic contradictions and structural imbalances?

The correct answers to the two questions will not only help people better understand China's ongoing economic cycle and its basic economic landscape, but will also help the country adopt right macroeconomic policies to deal with the ongoing economic slide.

China's economic slowdown for six consecutive quarters since the start of 2011 is by no means a temporary economic phenomenon. The blame should not be put on external factors, however. After more than three decades of fast economic growth, many officials, domestic enterprises and ordinary people have come to depend heavily on a fast-growing economy and are not psychologically prepared for China's transition from high-speed to normal growth. In this context, some people see the under-8 percent economic growth as increasing the risk of economic "hard landing".

As a matter of fact, China's GDP growth in the first half of this year is not only far higher than that of the US and European countries, but also outpaces such emerging economies as India, Brazil and Russia. In times of global economic disturbances, the nearly 8 percent economic growth rate is by any means a praiseworthy achievement.

For example, China's added industrial value grew by 10.5 percent year-on-year in the first half of this year, fixed asset investment by 20.4 percent and retail value by 14 percent - all three being within a reasonable range of growth. Although China's imports and exports during the same period declined considerably, its exports to the European Union fell by only 0.8 percent year-on-year. A lingering economic recession in the eurozone has caused some negative effects to China's economy, but it is not the main factor behind the country's continuing economic decline.

During a recent inspection tour of Jiangsu province, Premier Wen Jiabao said the decline of China's industrial output and profits has been caused mainly by overcapacity instead of a dwindling market share. "To stabilize growth is by no means a short-term countermeasure. Instead, it should be closely combined with the country's efforts for economic restructuring," Wen said.

A continuing economic decline in essence means that now is time for China to bid farewell to its fast-growth economic model. Under the influence of combined factors, ranging from the depletion of its population dividend and economic restructuring to its industrial upgrading and accelerated environmental protection since the 2008 global financial crisis, China's potential economic growth rate has declined from 9 percent to 8 percent.

However, a series of economic stimulus packages launched amid the global financial crisis prompted China's abnormal economic growth. The adoption of stimulus policies interrupted the country's economic restructuring efforts, too, and helped such overproduction industries as real estate, steel, ship-building and cement, thus fueling a new round of irrational growth.

The "marginal effect" produced by the country's investment and export-driven economic growth was given full play during the past decade but is now on the ebb. In comparison with a soft driving force behind the real economy, a boom in the real estate sector and soaring housing prices have further crippled people's purchasing power and hampered government efforts to boost domestic consumption.

A continuous economic slide once again proves that China's economic growth model, based on investment, exports and low value added manufacturing, has now become unsustainable. To put the blame of the country's economic slowdown on some external factors will only prompt the authorities to again come up with short-sighted measures to stabilize economic growth, which obviously cannot solve the fundamental problems facing the economy.

Government-spearheaded investment or loosened monetary policies cannot resolve the issues of overproduction, small and medium-sized enterprises' (SMEs) struggle for survival, application of excessive administrative power to economic activities, and monopoly and industrial upgrade.

The side effects of a large-scale economic stimulus package implemented by China four years ago prove that short-term economic growth measures - instead of profound reforms and structural adjustments - will sooner or later force the national economy into a bigger potential crisis.

To maintain a certain speed of economic growth the national economy should not be subjected to high-speed operation disregarding the law of economics. Most importantly, China has to be more tolerant toward economic deceleration and determined to eliminate backward industries, and take measures to alleviate tax burdens of enterprises, especially SMEs, to create a good environment for its overdue economic transformation.

The author is a Beijing-based economics commentator.

Copyright 1995 - 2010 . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()