|

|

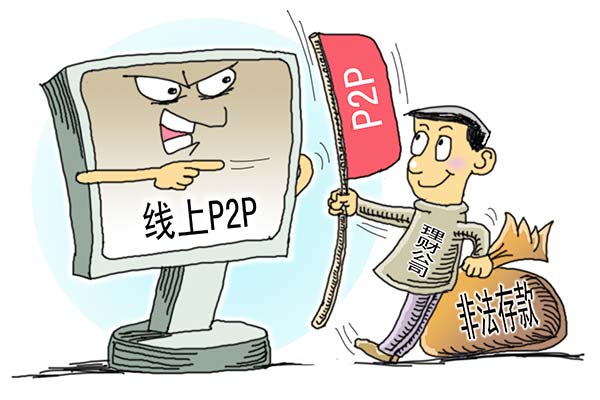

A cartoon showing offline finance companies that cheat investors in the name of P2P platforms.[Provided to China Daily] |

A news snippet about a con caught my eye last week. A Hangzhou court handed a life term to Cai Jincong for conning 1,200 investors.

His modus operandi was predictable: hard-sell a fashionable scheme, promise high returns (20 percent), raise money, disappear.

His firm, Zhejiang Yinfang Investment and Management Co, raised as much as 200 million yuan ($30 million) illegally. Cai spirited away 88 million yuan, peddling, well, investment products in the name of a peer-to-peer or P2P lending scheme.

Unlike regulated institutions such as banks, a P2P is basically an individual-or partnership-run online platform directly linking borrowers like startups with lenders who could be ordinary people.

China is said to be the world's largest P2P lending market with around 2,000 platforms. Their number shrank last year as many shuttered.

According to Chinese financial information providers such as Online Lending House, Wind Information and Caixin, a staggering 982 billion yuan was P2P-ed to borrowers last year, up from 253 billion yuan in 2014.

Since such loans are repaid relatively quickly, outstanding P2P debt was 439.5 billion yuan at the end of 2015, which rose to 576 billion yuan at the end of May. Evidently, business and technology go hand in hand.

And technology and fraud, too, are inseparable bedfellows, it seems. Computer viruses, hacking, phishing, credit card duplication, misuse of online passwords... you get the drift.

Every technological and financial innovation brings in its wake numerous risks like frauds whose scale could range from a few hundred yuan to billions of dollars.

Stock market manipulation, Ponzi schemes, interest rate rigging, dubious credit ratings, loaded analyst reports, imprudent bank loans, mis-selling of junk bonds, insurance policies and mind-boggling derivatives... all these seem inadequate lessons for investors.

These frauds have one thing in common: fraudsters' willingness to ruthlessly exploit gullible people's ignorance and weakness for fashionable concepts that ooze sophistication and legitimacy.

Look at the name of Cai's firm again. It has the words "investment" and "management". For the 1,200 investors duped by him, those words would have been very reassuring, creating the impression that the firm must be run by professional executives-experts with unimpeachable integrity.

Similarly, P2P has that ring of the modern-the in-thing. "Everyone is writing about it, must be safe, so jump on the bandwagon"-that could well have been the thinking of Cai's prey.

Small investors can't be faulted for thinking like that. For, at their level, and in this digital-social era, media usually are the main source of information.

With so much being made of startups, innovation, venture capitalists, private equity, crowdfunding and what not, lenders may be forgiven if they decide to turn a little more enterprising and imaginative.

After all, how many can resist the temptation of high returns, given the recent volatility and risk in traditional gambling dens like securities and currency markets? And, isn't P2P fashionable, preferable, even noble?

Funding startups via P2P, you know, could help create the next Alibaba, strengthening innovation, China's current obsession. It could also make one rich, should the startup hit pay dirt and reward its investors.

Well, thin, blurry lines separate the bands of ignorance, naivete, good intention and greed in the small-investment spectrum.

Small investors in relatively mature financial markets like the US may be more aware and better protected now, after the earth-shaking scandals there. But the same cannot be said of retail investors in developing countries like China and India (where I come from).

As P2P platforms mushroomed, India's central bank, sensing potential risks, said it will consider bringing them under its ambit. Countries like Israel and Japan have banned them altogether, while the UK is mulling tighter regulations.

After years of talk of P2P regulation, the authorities concerned in China proposed draft rules on Dec 28. The hands-off approach lays stress on risk controls and self-regulation, so that alternative sources of funding for millions of capital-starved businesses don't get choked by rules.

Now, however, Cai's con job could give fresh ammunition to those who want tighter regulations to rein in scammers who retain money without passing it on to borrowers or raise money to fund fictitious startups.

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 130349 ![]()