|

A clerk from a rural credit cooperative in Linyi, Shandong province, counts banknotes. [Photo/bjreview.com.cn] |

State-owned lender China Construction Bank Corp is in talks with the People's Bank of China, the central bank, for a possible liquidity injection under the standing lending facility of the latter, its Chairman Wang Hongzhang said on Friday.

Rumors began to spread on Tuesday that the central bank would provide funds totaling 500 billion yuan ($81.5 billion) via SLF to five major State-owned commercial banks, including the CCB.

"The 500 billion yuan SLF is part of the prudent monetary policy of the People's Bank of China," Wang said. "It should not be regarded as a change in the direction of the monetary policy or a strong stimulus to the economy.

"We'll get a part of the 500 billion yuan from the PBOC in times of financial strain, but we have not yet seen the need to do so. Even if the PBOC releases 500 billion yuan into the market, the liquidity injection would not have a huge impact because domestic banks in general, whether large or small, do not have a liquidity problem, and money market rates have not gone up," he said.

The CCB will observe and evaluate the impact of the fund injection on increasing liquidity and in enhancing scientific allocation of capital, he said.

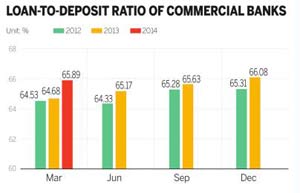

As the economy is slowing down, many bankers and economists have urged the banking regulator to remove the 75 percent cap on the loan-to-deposit ratio to spur growth. The cap had been implemented as a measure to reduce lending risks.

"I personally believe that the regulation on the loan-to-deposit ratio can either be continued or relaxed. The key is to set a different evaluation index on loan-to-deposit ratios for different banks according to their management abilities, risk awareness and operational conditions, instead of imposing non-discretionary rules for all banks," Wang said.

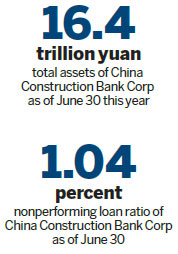

As of June 30, the CCB had total assets of 16.4 trillion yuan, with a core Tier-1 capital adequacy ratio of 11.21 percent. Its nonperforming loans increased to 95.7 billion yuan from 85.3 billion yuan on Dec 31 and the NPL ratio went up 5 basis points to 1.04 percent.

The bank's bad loans mostly occurred in the manufacturing, retailing and wholesaling industries in Zhejiang, Jiangsu and Shandong provinces.

"More than 80 percent of our bad loans occurred in small and micro enterprises. It had something to do with our operation model as in the past we offered a considerable amount of funding to businesses as long as they had mutual loan guarantees rather than requiring them to provide collateral," Wang said.

At present, collateral loans account for slightly more than 50 percent of the bank's total lending. The CCB will strive to increase that percentage, he said.

In an effort to reduce bad loans, the bank is trying to build multi-business connections with clients by requiring small companies that want to receive loans to open a full range of accounts at the bank, rather than just focusing on attracting their deposits. It will also strengthen efforts to examine the clients' actual financial conditions.

In addition, the bank has also accelerated the disposal of its bad loans. It has sold bad loans in packages worth 5-6 billion yuan and has written off even more this year. It will take some time for all these efforts to bear fruit as the economy still faces downward pressure, Wang said.

|

|

| PBOC acts to shore up liquidity | Starting now, bank loans easier to get |

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()