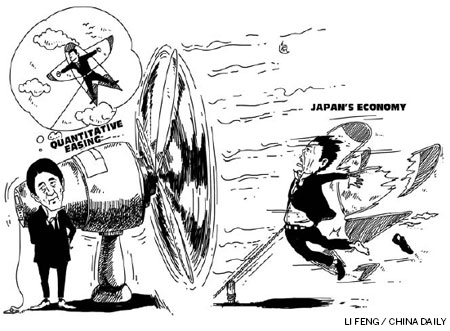

The politicization of central banking continues unabated. The resurrection of Japanese Prime Minister Shinzo Abe and Japan's Liberal Democratic Party, pillars of the political system that has left the Japanese economy mired in two lost decades and counting, is just the latest case in point.

Japan's recent election hinged critically on Abe's views on the Bank of Japan's monetary policy stance. He argued that a timid BOJ should learn from its more aggressive counterparts, the US Federal Reserve and the European Central Bank. Just as the Fed and the ECB have apparently saved the day through their unconventional and aggressive quantitative easing (QE), goes the argument, Abe believes it is now time for the BOJ to do the same.

It certainly looks as if he will get his way. With BOJ Governor Masaaki Shirakawa's term ending in April, Abe will be able to select a successor, and two deputy governors as well, to do his bidding.

But will it work? While experimental monetary policy is now widely accepted as standard operating procedure in today's post-crisis era, its efficacy is dubious. Nearly four years after the world hit bottom in the aftermath of the global financial crisis, QE's impact has been strikingly asymmetric. While massive liquidity injections were effective in unfreezing credit markets and arrested the worst of the crisis, witness the role of the Fed's first round of QE in 2009-2010, subsequent efforts have not sparked anything close to a normal cyclical recovery.

The reason is not hard to fathom. Hobbled by severe damage to private and public sector balance sheets, and with policy interest rates at or near zero, post-bubble economies have been mired in a classic "liquidity trap." They are more focused on paying down massive debt overhangs built up before the crisis than on assuming new debt and boosting aggregate demand.

The sad case of the American consumer is a classic example of how this plays out. In the years leading up to the crisis, two bubbles property and credit fueled a record-high personal-consumption binge. When the bubbles burst, households understandably became fixated on balance-sheet repair, namely, paying down debt and rebuilding personal savings, rather than resuming excessive spending habits.

Indeed, notwithstanding an unprecedented post-crisis tripling of Fed assets to roughly $3 trillion, probably on their way to $4 trillion over the next year, US consumers have pulled back as never before. In the 19 quarters since the start of 2008, annualized growth of inflation-adjusted consumer spending has averaged just 0.7 percent, almost three percentage points below the 3.6 percent trend increases recorded in the 11 years ending in 2006.

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 130349 ![]()