In early August, the long-bearish market had a brief rally as investors cheered the highest manufacturing Purchasing Managers Index for July in more than two years.

But within days, the market was falling after a private gauge of service activity sank to a record low and concerns over the property market re-emerged.

Analysts are quick to point out that investors have been disappointed by the absence of further credit easing. But the thirst for additional stimulus measures also underscored the fragility of the current recovery.

Financial institutions have noted that the manufacturing PMI's improvement since March was essentially the result of credit easing. In June, banks made $174 billion of new yuan loans, nearly 20 percent above market expectations. Credit numbers for July are due this week, and analysts expect a record high for that month.

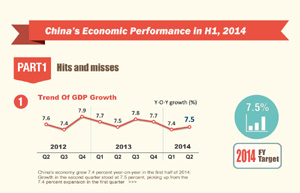

In early 2013, the term "Likonomics" coined by Barclays Capital went viral. It summarized the new Premier Li Keqiang's policy as "no stimulus, deleveraging and structural reform". Now the word is barely seen in the Chinese press, as policy priorities have quietly shifted to safeguarding the 7.5 percent GDP growth target.

The reality is "deleveraging" did not take place in the past two years. According to Standard Chartered Plc's estimate, the ratio of total debt to GDP swelled from 147 percent at the end of 2008 to 251 percent at the end of June this year. By comparison, the United States and the United Kingdom, two much richer countries, have ratios of 260 percent and 277 percent, respectively.

With the broad measure of money supply (M2) mounting to 120.96 trillion yuan by the end of June, China is awash in money. At the same time, private companies keep complaining that it is tough for them to borrow from banks.

When they turn to nonbank channels, the cost of borrowing is painfully high: usually above 15 percent for a one-year loan. Economists have many explanations for this state of affairs, but it underscores the unusually low efficiency of the financial system.

A more acute and worrying fact is that skyrocketing credit is having a decreasing impact. In 2007, total social financing, the broadest measure of credit supply, was 5.96 trillion yuan, and GDP grew 13 percent that year. During the first half of this year, 10.57 trillion yuan was unleashed (whole-year TSF is expected to exceed 20 trillion yuan), but growth dipped to 7.4 percent. Even considering that the nation's GDP in 2013 was 2.12 times that recorded in 2007, the fall in efficiency is significant.

Analysts are also worried that with liquidity easing again, "zombie" enterprises, once at the edge of extinction, could survive to function for another day. Inefficient State-owned enterprises in sectors with excess capacity and wasteful local government financing vehicles could sustain the credit binge. The ongoing correction in the property market that could create a healthier structure may end up going nowhere as struggling developers grab financial lifelines again. For the moment, China cannot seem to shake its credit addiction.

You cannot pursue a sudden, sharp "deleveraging" in an economy that is not growing. Central leaders know that well. But with the fast expansion of debt continuing and limited reform measures in sight, people are wondering if the leveraging is sustainable.

Compared with the central government, local governments have showed even less interest in finding an alternative path. Responding to the slowdown in the first half, many local governments are rolling out their own visions of "stimulus".

The combined investments they have vowed to make have surpassed 6 trillion yuan, according to Economic Information Daily.

Leaving aside where they can get such sums, the bigger problem is: investment is still seen as a convenient way to sustain growth without thinking about the long term. For example, northeast Heilongjiang province announced a two-year plan for 300 billion yuan in investment, mostly in infrastructure and mining, after its growth dipped to 4.8 percent in the first half, the lowest among all provincial-level regions.

However, the major cause of the slowdown was that a large oilfield, which generated half of the province's industrial output and nearly one-third of its GDP, was hit hard by decreased production. Did local officials give any hint how the economy would reduce its reliance on that oilfield?

|

|

|

| Infographic: China's economic performance in H1, 2014 | China's economy to grow 7.5% in 2014: IMF |

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 20100000002731 ![]()