Gray area

One of the main reasons that last year's default in the city was so hard to rein in is that until recently there was no reliable data to show how many loans are out there and how high the rates are.

"Private lending in Wenzhou is a gray area. There are no data on it and nobody knows its size," said Zhou Dewen, chairman of the Wenzhou SME Development Association. "The center will help to bring the city's private lending above ground, and that will help with risk control."

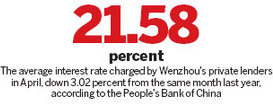

In fact, after the launch of the center, the Wenzhou branch of the People's Bank of China, the central bank, has started to report the average interest rates of Wenzhou's private lending on a monthly basis. In April, the average was 21.58 percent, down 3.02 percent from the same month last year and 0.08 percent from March, according to the report.

Despite close media attention, the center wasn't a runaway success initially. Although capital of more than 1 billion had been registered by May 15, only 7 million yuan was actually lent out. More than 100 people visit the center every day, but few actually strike deals, Xu added.

|

|

Previously, Xu would lend money to acquaintances through verbal contracts. But following the events of last year, he now demands collateral for every penny he lends, he said.

"I'm in no hurry. I'm just checking this place out. Safety is key nowadays," he said.

Borrowers, however, are more eager, but often find the loan conditions too demanding. "They are asking for too much collateral. But if I already had enough, I would have gone to the banks," said Zheng Ran, the owner of a small business. "I am willing to pay higher rates to lenders, but it's not allowed."

Zheng's frustration highlights a serious problem with the center: Why would private lenders work in a more transparent setting, when they can conduct their highly profitable business while remaining underground?

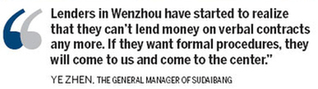

However, Ye Zhen, the general manager of Sudaibang, said many "gray lenders" will make the move, especially after the massive defaults last year raised risk-awareness in the city. "Lenders in Wenzhou have started to realize that they can't lend money on verbal contracts any more. If they want formal procedures, they will come to us and come to the center," said Ye.

Reluctant to lend

However, Wenzhou's private lenders have already become more reluctant to lend. A recent survey by the city's banking regulator shows that scale of private lending is currently 30 percent lower than in August, as lenders grow more cautious.

But disputes are growing. Legal cases concerning private lending in the city increased 89 percent year-on-year in the first four months of this year, according to Wenzhou Intermediate People's Court on May 21.

Xu, the center's president, said it is reasonable that people will be cautious about the center at the beginning, but things will gradually get on track. He expects the monthly transaction volume to reach at least 100 million yuan in the near future.

|

The stakes involved in the center are high because it's the first step in Wenzhou's financial reforms. If the center proves a success, it will probably affect the way that the central government pushes ahead with other measures in the pilot. If it's unsuccessful, the chances are slim that it will be expanded to other parts of the country.

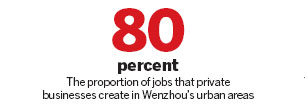

The reforms are urgently needed. China's current banking monopoly by State-owned lenders, which Premier Wen Jiabao has vowed to break, leads to low interest rates on deposits and makes credit scarce for SMEs. The monopoly effectively taxes depositors and distorts the distribution of financial resources nationally. While inefficient State-owned enterprises revel in easy loans, private businesses, which create 80 percent of the jobs in urban areas, often find potential business-saving credit hard to obtain.

Many experts believe that the nation's backward financial system is choking the vigor of the real economy. Pu Haiqing, a deputy of the National People's Congress, said during the annual "two sessions" (meetings of the NPC and the Chinese People's Political Consultative Conference) in March, that the banking sector's "exorbitant profit" blunts the nation's competitive edge and the development of the real economy.

Lai Xiaoxuan, deputy general manager of Zhejiang Topsun Holding Group, which makes outdoor sporting equipment, said his company could have grown much more quickly if bank loans were more easily accessible. "We are building a design center in Europe. A lack of funding is one of the main reasons that we didn't move faster," he said.

At a time when domestic economic growth is slowing and external demand shows no sign of picking up, funding is even more important for private businesses to help them weather the hard times, he added.

Back at the month-old private lending center, Xu Zhiqian was taking a last walk around before leaving the office at the end of the day. "I am confident about the future of the center," he said. "There is demand and there is supply - all that's needed is a suitable way of connecting them."

Contact the reporter at gaochangxin@chinadaily.com.cn

Copyright 1995 - . All rights reserved. The content (including but not limited to text, photo, multimedia information, etc) published in this site belongs to China Daily Information Co (CDIC). Without written authorization from CDIC, such content shall not be republished or used in any form. Note: Browsers with 1024*768 or higher resolution are suggested for this site.

License for publishing multimedia online 0108263 Registration Number: 130349 ![]()