Call to include foreign assets in portfolio

Despite the strong domestic equity market performance coupled with expectations of a renminbi appreciation, Chinese institutional investors should consider investing offshore to improve expected risk-adjusted returns.

According to a recent report by transnational Mercer Investment Consulting, Chinese institutional investors are increasingly able to diversify their portfolio exposures through greater use of QDIIs (qualified domestic institutional investors), which can be used to leverage market risks.

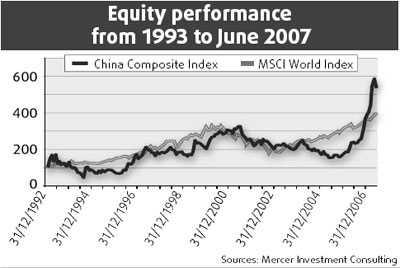

The recent growth of the A-share market in China has been spectacular. Between 1993 and 2007, the Chinese equity market outperformed markets of the developed world, rising by 12.6 percent annually, while the figure for the global equity index was 10 percent.

However, this magnificent performance was entirely due to the dramatic rise of the Chinese market over the last 18 months. Till 2005, global equity markets achieved 9.2 percent annual growth over the previous 13 years, while the China Composite Index, which tracks A shares listed in Shanghai and Shenzhen, rose only 3.8 percent.

Chinese equity markets have been considerably more volatile than developed global markets. Mercer expects the volatility of Chinese equities will continue to be higher than global equities, and views volatility as a reasonable measure of the uncertainty or risk of future investment outcomes.

Despite the higher-than-expected return from local equities, Chinese institutional investors who are risk-averse may prefer to include global developed market equities in their portfolios.

The report indicates that inclusion of global equities has less to do with returns and more to do with the potential benefits of reducing risks.

Economists and market participants expect the yuan to appreciate over time relative to the US dollar, although there is a difference of opinion about the speed and extent of such an appreciation.

Mercer says it has surveyed more than 30 investment management firms about their expectations as to the "fair" value of the yuan. They believe the US dollar will depreciate against the yuan by 10 percent over the medium term and the euro and the pound are expected to depreciate against the US dollar while the Japanese yen will appreciate.

This, compounded with greater equity return expectations from the Chinese market than the global market as a whole over the long term renders global asset classes less attractive to Chinese domestic investors.

However, the lower expected return volatility of global equity markets, relative to Chinese equities, means that global equities still have a place in China's domestic portfolio.

Moreover, the relatively low correlation of global and Chinese asset classes implies a diversification benefit from investing in these asset classes.

The consulting firm supports the view that Chinese investors will benefit from greater freedom to invest overseas.

The risk reduction afforded by such diversification allows for a greater allocation to riskier asset classes, particularly equities, for a given risk tolerance.

"Of course, there is a risk that the speed of renminbi appreciation in the short term might be higher than that implied," said Garry Hawker, of Mercer Investment Consulting. "However, this risk is to an extent mitigated by the likelihood that it would take some time to build up an exposure to global equities of some size."

He believes it will also be important to stress-test asset allocations to more extreme levels of appreciation.

(China Daily 10/19/2007 page15)