Where next for the ChiNext?

Updated: 2011-09-28 09:14

By Gao Changxin (China Daily)

|

|||||||||||

|

|

After a grand debut in 2009 and a notable rally last year, the ChiNext board - an exchange for high-growth, high-tech start-ups - has undergone a major retreat this year.

To make matters worse, analysts say the decline of the Shenzhen Stock Exchange's counterpart to the Nasdaq is not due to normal cyclical fluctuation. Rather, they believe that it represents the bursting of a bubble as investors return to rationality.

Worse, the experts have warned that the downward trend could continue, as global and European uncertainties take a toll on the domestic market, especially small-cap companies.

The scale of the retreat has been phenomenal. The ChiNext had shed a third of its value, sliding from a high of 1239.6 on Dec 20 to a record low of 783.86 in intraday trading on June 23.

By comparison, the Shanghai Composite Index, which tracks the bigger of China's stock exchanges, dropped only 5.26 percent from 2825.33 on Jan 1 to 2664.28 on June 16.

Back then, 120, or 54.3 percent, of the 221 stocks on the ChiNext had fallen below their issue price. Among them, 101 stocks were trading at more than 30 percent lower than their debut levels.

The board, which has a lower listing threshold than other indexes, offers riskier but potentially more profitable investment opportunities, and imposes more stringent rules on trading, disclosure of information and delisting.

Unlike investors on the main board, those focusing on the ChiNext often look not at how much the companies are earning at the present time, but at their future growth and potential profitability.

Analysts say that one indication that the board is overvalued is that it has an ultra-high price-to-earnings ratio, a measure of the market's expectation of future earnings growth.

The board's average ratio reached a high of 80.01 this year, before slumping to around 40.

That figure is more than twice that of the A-share market and the New York-based Nasdaq. On June 17, the average price-to-earnings ratio of A-share stocks was 15.76, while the rate for Nasdaq stocks was below 20.

"We have always said that the high price-to-earnings ratio for the ChiNext was unsustainable and a sign of overheating. Now it's been halved to 40, and I think there is further room for adjustment," said Lei Zhonghui, an investment manager with the Zero2IPO Group, a Chinese venture-capital (VC) company.

"The decline in the price-to-earnings ratio is confirmation of our view that many ChiNext stocks are overvalued. The high ratio suggests that the board's companies have great growth potential, which they actually don't," said Lei.

Much of the decline came after investor confidence was dented by the sluggish results reported by the board's companies in the first quarter of this year.

During that period, 23 percent of the 221 ChiNext companies reported a decline in net profit, according to Heading Century Consulting Co Ltd, an IPO consulting firm. And 12 of the 56 companies that have joined the board this year reported a decline in profits.

For example, Xinning Modern Logistics Co Ltd lost 1.81 million yuan ($283,700) in the first quarter, compared with a profit of 2.35 million it registered in the same period a year ago.

Meanwhile, Ningbo GQY Video & Telecom Joint Stock Co Ltd, a maker of video products, saw its first-quarter profit plummet more than 90 percent from 8.51 million yuan in the same period in 2010.

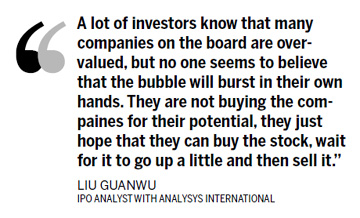

"Investment banks and venture capital firms, which benefit from high issue prices, are behind the board's overvaluation," said Liu Guanwu, an IPO analyst with Analysys International, a Beijing-based consulting firm.

He said investment banks and VC companies will use financial and administrative measures to 'package' companies before their IPOs, in a move to convince investors that a company has great growth potential and deserves a high valuation.

"The higher the issuing price, the higher the commission gained by the investment banks and the return for venture capital, so they have an incentive to push up the issuing prices," Liu said.

For some companies, even the managements themselves seem to have little faith in their company's future, selling their stock immediately after the lock-up period expired.

According to figures from the Shenzhen Stock Exchange, 21 companies on the board were shorted by their own managements in May. And as of May, only 79 ChiNext companies had been listed for longer than the one year lock-up period required before management could sell the stock.

Heading Century said in a recent report that irregularities have been rampant in ChiNext IPOs. Since the board's launch, regulators have received 200 written accusations concerning more than 100 companies, it said.

"The accusations touch on irregularities in equity transfer, affiliated transactions, taxation and patents, exposing the phenomenon that some companies engage in fraud in their IPO processes," Heading Century said in the report.

For now, VC companies, which make a profit out of exits from IPOs, seem to be the biggest beneficiaries of the ChiNext. As of May 30, 134 of the 221 companies on the board were backed by VCs, according to Analysys International.

The board's exceptionally high price-to-earnings ratio, providing exit channels with high returns, has led to a better investment return for VC firms.

The average return on VC/Private Equity investments on the ChiNext stood at 11.59 times, compared with a return of 5.91 times on foreign stock markets, Ni Zhengdong, president of Zero2IPO, told a forum in Shanghai last year.

Related Stories

ChiNext Index closes higher - Sept 27 2011-09-27 16:37

ChiNext Index closes down -- Sept 26 2011-09-26 17:10

ChiNext Index closes down - Sept 23 2011-09-23 16:42

ChiNext Index closes down - Sept 22 2011-09-22 16:40

- Chinese businesses want a wider door to the US

- Imported iron ore supplies decline in China

- Legend bulks up to get ready for listing

- Trade zone projects on border 'going well'

- Liquor makers ordered to stabilize prices

- China's auto exports surge 53.3% in Jan-July

- China propels Huawei's sales

- Where next for the ChiNext?