OPINION> OP-ED CONTRIBUTORS

|

OPINION> OP-ED CONTRIBUTORS

|

|

What makes a global financial center

By Andrew Sheng (China Daily)

Updated: 2009-08-14 07:45

We grow up thinking the world is balanced - that good cancels out evil, that assets equal liabilities, that life is a simple bell-shaped curve. But that's not the case. There is a lot of inequality in the world. We like buying, but we do not sell that often, except when forced to. Risks in the financial world are similar. George Soros recently consolidated my belief in the saying, common sense is not so common. Financial markets are dangerous because the risk of going long (only buying and not selling) is not the same as going short (selling or borrowing what you don't have). If you buy something and the price drops to zero, all you lose is your asset. But if you borrow or you go short on a product, you could not only lose everything you have, but also end up owing far more than you realize. This is the common sense AIG failed to appreciate. If you insure cars or life, you are working with the law of large numbers. As long as your premium covers the estimated losses, you can still make money. But if you insure banks (which are highly leveraged institutions) or borrowers, exactly what AIG's derivative trading subsidiary did in London, the losses will be amplified by the embedded derivatives. Imagine someone trying to insure the recent global bank losses of nearly $3 trillion. The banks lost a lot because they were highly leveraged institutions. The lower the price of assets that they hold, the greater their bankruptcy. So AIG needed more than $180 billion to bail itself out, compared with the initial request for only $10 billion. This takes us back to the use of a country's currency as international reserve currency (which we discussed last week). When a currency circulates within the borders of just one country, it is a case of one citizen lending to another, or the left hand borrowing from the right. If someone does not pay his or her debt, there are laws to protect the lender. Even if the corporate sector over-borrows and collapses, the state can intervene by either nationalizing the debt or taxing the rest of the population to pay for the losses.

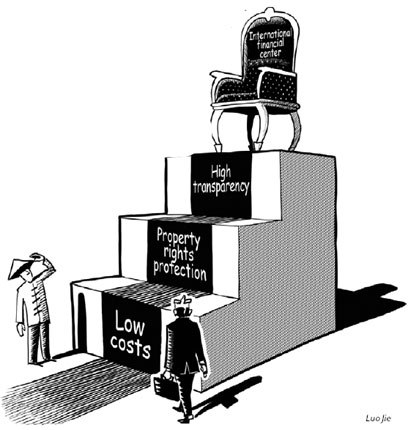

Asians have not forgotten that in the 19th century foreign debt was imposed on them through gunboats and military invasions. It is not good to have too much foreign debt because a central bank cannot print foreign currency. So why should a country want its currency to be an international reserve currency? There are two basic reasons for that. The first is seigniorage, which means anyone who issues currency is actually borrowing money without interest. All central banks earn seigniorage by issuing currency. In a sense, it is the premium citizens pay to the central bank for safeguarding the value of their currency. Therefore, the country that issues a global reserve currency enjoys seigniorage from foreigners who hold its currency. This amount can be very large indeed, as in the case of the US. But the actual benefits received for trade and commercial services when the currency is the reserve standard are larger. In the days of the British Empire, London benefited hugely from being the financial center for the pound sterling, as well as the trading hub for commodities, international loans and related legal and commercial services. Although the sterling lost its role as a major reserve currency to the US dollar, London became the center for the offshore euro-dollar market and also an important complement to New York. The biggest commercial banks, brokers, fund managers and insurance companies were located both in London and New York because they shared the same language and similar laws and business practices. So what makes an international financial center? After working in Hong Kong, I finally understood that an international financial center must meet three basic conditions: protect property rights, have lower transaction costs, and have high transparency. The first condition is obvious and yet not so obvious. Most Western economists say London and New York have superior property rights because they have well-accepted common laws and excellent and fair judiciaries. But protection of property rights is more than just laws and enforcement. Protection of property rights also means political stability, and the absence of nationalization, predatory taxation and a strong military power. To put it bluntly, no successful international financial center operates in a war zone or a banana republic. The second condition, of low transaction costs, is very important. No financial center will succeed if it is not convenient to do business there with low regulatory costs and good communications infrastructure. The best financial centers have excellent telecommunication and transport networks and living conditions. Transaction costs are associated with geography, too. It is no coincidence that New York dominates in the American time zone and London in the European and African time zones. Asia has no dominant financial center for reasons that I will discuss later. High transparency is needed because markets thrive on information. If information is not accurate, timely and accessible, investors will not know how to protect their funds and make good decisions. Next, I shall look at why Japan failed to make yen a dominant global reserve currency. The author is Adjunct Professor in Tsinghua University, Beijing, and University of Malaya. He is a former chairman of Hong Kong's Securities and Futures Commission. (China Daily 08/14/2009 page9) |