|

|

G20 London Summit > Top News

|

Stability, growth, jobs = $1 trillionBy Bao Daozu (China Daily)

Updated: 2009-04-03 07:29 LONDON: The Group of 20 leaders yesterday pledged an additional $1.1 trillion to restore credit, growth and jobs in the world economy, announcing a broad raft of measures designed to hasten the end of the global financial crisis.

They also declared a crackdown on tax havens, regulation of hedge funds and a new supervisory body to flag problems in the world financial system. The host, British Prime Minister Gordon Brown, said:"Today, the largest countries of the world have agreed on a global plan for economic recovery and reform."

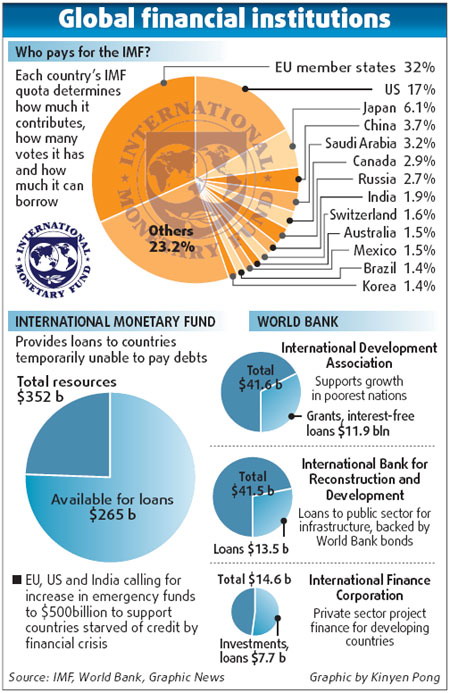

All the major indices were trading at more than 3.5 percent at mid-day with optimism that the country's economy was on the mend. In London, the FTSE 100 index of leading British shares closed more than 4 percent higher following the announcement of the summit deal. In a sweeping G20 communique, the world leaders vowed to join hands to spur the global economy, repair the financial system, strengthen global financial regulation, battle trade protectionism and achieve green and sustainable recovery. They promised "an unprecedented and concerted fiscal expansion" to create jobs, raise output by 4 percent and push for the world's shift to a green economy, according to the Leaders' Statement released at the end of the G20 London Summit. They agreed to triple the IMF resources to $750 billion, which coupled with new special drawing rights, additional lending and guarantees for trade finance, will provide the world with an additional $1.1 trillion program to "restore credit, growth and jobs" in the world economy. China has pledged to extend $40 billion to enlarge IMF resources, Brown said at the press conference immediately after the leaders signed the statement. To strengthen financial supervision and regulation, the leaders agreed to establish a new "financial stability board" (FSB) with a strengthened mandate, as a successor to the existing financial stability forum (FSF), joined by all G20 members. FSB will collaborate with the IMF to provide early warnings of macroeconomic and financial risks and the actions needed to address them. "This is the day the world came together to fight back against the global recession. Not with words but a plan for global recovery and for reform and with a clear timetable," Brown said. The leaders also set principles to reform the international banking system. "This is a comprehensive program of measures that includes, for the first time, bringing the shadow banking system, including hedge funds, within the global regulatory net," he said. The leaders expressed their commitment to reaching an ambitious and balanced conclusion to the Doha Development Round, to give the global economy an estimated boost of $150 billion a year, the statement said. They also pledged to "lay the foundation for a fair and sustainable world economy" and help the poorest countries achieve the millennium development goals.

|

|