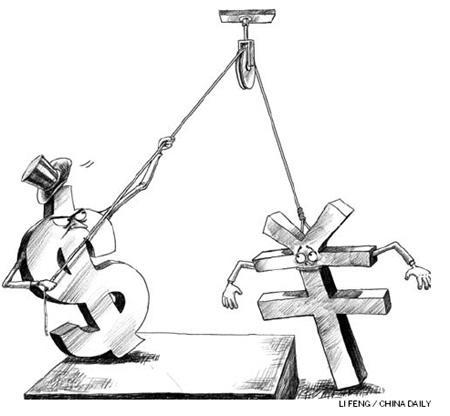

Op-Ed Contributors

Tagging the yuan as a scapegoat is unfair

(China Daily)

Updated: 2010-03-24 07:48

|

Large Medium Small |

Editor's note: Beggar-thy-neighbor currency protectionism, which played a central role in the collapse of world trade in the 1930s, will come back if the West do nothing but blame China, the Wall Street Journal article pointed out.

As if the world economy wasn't fragile enough, politicians in the United States and China seem intent on fighting an old-fashioned currency war. The US is more wrong than China here, and it's important to understand why, lest the two countries send the world back to the dark age of beggar-thy-neighbor currency protectionism.

The battle concerns China's decision to peg its currency, the yuan, to a fixed rate of roughly 6.83 to one US dollar. To hear the American political and business establishment tell it, this single price is the source of all global economic problems. The peg keeps the yuan "undervalued" in this telling, fueling China's exports and harming the US, Europe and everyone else. If the Chinese would only let the yuan "float," it would soar in value, China's export advantage would fall, and the much-despised "imbalances" in global trade would end.

|

||||

At the core of this argument is a basic misunderstanding of monetary policy. There is no free market in currencies, as there is in wheat or bananas. Currencies trade in global markets, but their supply is controlled by a cartel of central banks, which have a monopoly on money creation. The Federal Reserve controls the global supply of dollars and thus has far more influence over the greenback's value than any other single actor.

A fixed exchange rate is also not some nefarious economic practice rare in human affairs. From the end of World War II through the early 1970s, most global currency rates were fixed under the Bretton-Woods monetary system created by Lord Keynes and Harry Dexter White. That system fell apart with the US-inspired inflation of the 1970s, and much of the world moved to "floating rates."

But numerous countries continue to peg their currencies to the dollar, and with the establishment of the euro most of Europe decided to move to a fixed-rate system. The reason isn't to get some trade advantage against their neighbors but to gain the economic benefits of stable exchange rates - and in some cases a more stable monetary policy. A stable exchange rate eliminates a major source of uncertainty for investment decisions and trade and capital flows.

The catch is that under a fixed-rate system a country yields some or all of its monetary independence. In the case of euro-bloc countries this means yielding to the European Central Bank, and for dollar-bloc countries to the US Federal Reserve.

This is what China has done with its yuan peg to the dollar. By maintaining a fixed yuan-dollar rate, China has subcontracted much of its monetary discretion to the Fed in return for the benefits of exchange-rate stability. For more than a decade, this has served the world economy well, leading to an explosion of trade, cheaper goods for Americans that have raised US living standards, and new prosperity for tens of millions of Chinese.

For years, the US establishment has nonetheless been pressing China to "revalue" the yuan in the name of reducing the US trade deficit. Never mind that much of this deficit is intra-company trade, with US companies outsourcing production to China to stay globally competitive (and their US workers and shareholders profiting). Beijing bent for a while in the middle of the last decade and adopted a crawling peg that revalued the yuan by about 18 percent, but that had little impact on the trade deficit. China re-fixed the peg amid the financial panic of 2008, and now the American "revalue" clamor is rising again.

China is right to resist these calls, not least because a large revaluation could damage China's growth. China has learned from the experience of Japan, which bowed to similar US currency pressure in the 1980s and 1990s, revaluing the yen from 360 to the dollar to as high as 80 in 1995. As Stanford economist Ron McKinnon has shown, one result was domestic deflation in Japan and its lost decades of growth. Meanwhile, Japan continued to run a trade surplus, as imports fell with slower internal growth and cross-border prices adjusted. China has helped to lead the global economy out of this recession, and the world needs that to continue.

One proposed alternative is for China to once again move to a crawling peg, with a modest revaluation. But that would only invite more pressure on the yuan, as global "hot money" and currency speculators anticipate a further yuan rise. This is especially true with the Fed keeping dollar interest rates at zero, which also encourages more hot money into China in anticipation of a rising yuan.

This is not to say that the current arrangement is ideal. China's real problem isn't its peg to the dollar but the yuan's lack of convertibility to other currencies and capital controls. These controls have blunted the yuan's development as a tradable currency, which means private markets can't recycle the flow of dollars into China from its large trade surplus. Instead, the job is left to China's central bank, which buys dollars deposited in Chinese banks with yuan. This is why the central bank has accumulated some $2.5 trillion in dollar reserves.

China's build-up in dollar reserves is contributing to the world's anger at China, and it represents a huge misallocation of global resources. Instead of letting its dollar reserves find their best private investment use, China uses them to buy US Treasury bills or Fannie Mae securities.

One solution would be to make the yuan convertible, and let capital and trade flows adjust through private markets rather than the Chinese central bank. This is how Germany recycles its trade surplus. A one-time small revaluation to, say, 6.5 yuan to the dollar accompanied by convertibility would help with global adjustment while avoiding the perils of Japan-like deflation.

The Chinese government resists open capital markets because it fears less political control. At least at first a convertible yuan might also lead to a surge in capital outflows from China as Chinese companies and individuals diversified their currency holdings and investments. But over time, and probably quickly, markets would adjust and reach a new equilibrium. Convertibility would also increase the domestic pressure for China to further liberalize its financial system.

This is where the US should put its diplomatic pressure, rather than on the exchange rate. Even better would be a joint US Treasury-Chinese declaration on behalf of such a policy shift, which would give credibility to the new monetary arrangement.

We realize these views diverge from the current US establishment's patent medicine of smacking China and devaluing the dollar. But we hope they at least introduce a note of caution into the drive to blame the yuan and China for America's current run of economic anxiety.

It's especially dismaying to see the same US and European economists and columnists who peddled Keynesian stimulus as an economic cure-all now tell us that their policies would be working better if only the yuan-dollar price were different. Because their own ideas have flopped, they now want to make the yuan a scapegoat and risk a trade war with China. Haven't they done enough harm already?

Editorial reprinted from March 18 edition of The Wall Street Journal, Dow Jones & Company, Inc. All rights reserved

(China Daily 03/24/2010 page9)