Economic expectations up after two sessions

China has set its main targets for economic and social development and budget plans in the Government Work Report, presented during the two sessions that ended earlier this month.

It is expected that more policies will gradually be put into practice and the country will fulfill expectations.

Such efforts are actually in line with the country's vision outlined at the Central Economic Work Conference last December, where the leadership vowed to effectively enhance economic vitality, prevent and resolve risks, improve social expectations, and consolidate the positive momentum of economic recovery.

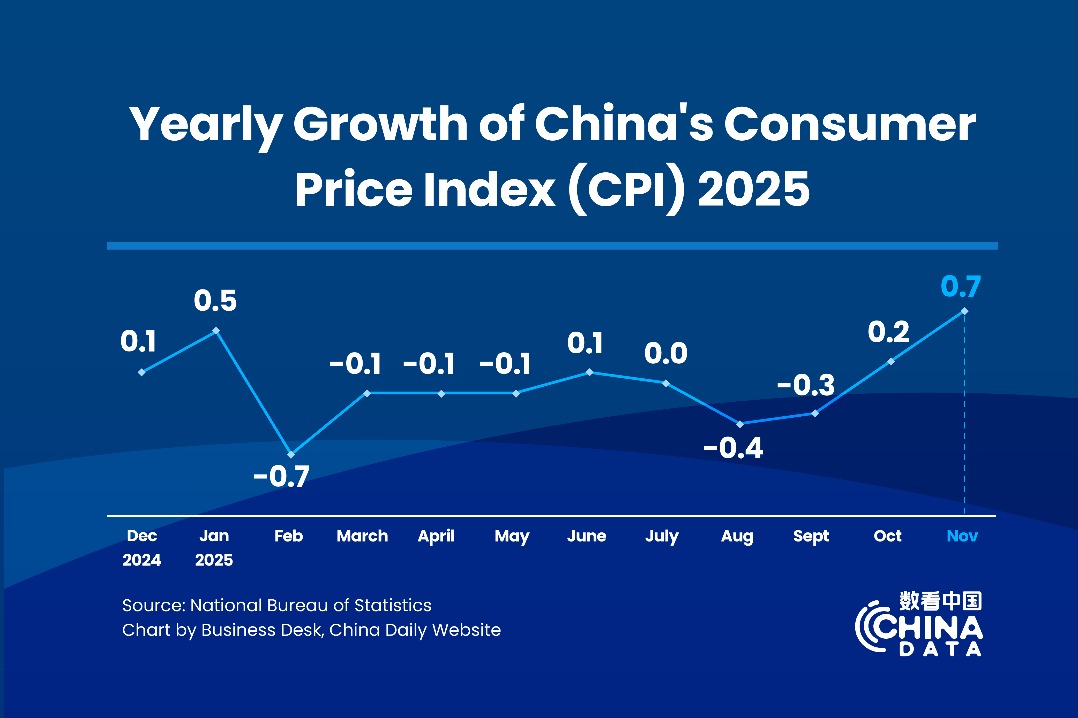

The 5 percent economic growth target for this year set in the Government Work Report is generally in line with market expectations. If consumer prices can rise moderately this year and push the GDP deflator from negative to positive, nominal GDP is expected to exceed real GDP again.

The growth target has sparked heated discussions at home and abroad.

The International Monetary Fund, the World Bank, the United Nations and the Organization for Economic Cooperation and Development have forecast the Chinese economy will grow in the range of 4.5 percent to 4.7 percent this year, citing factors such as adjustments in the real estate industry, inadequate social security, weak external demand and tense trade situations.

Though it will not be easy for China to achieve its growth target this year, the Chinese government has a clear roadmap. The Government Work Report, while affirming achievements, has also pointed out difficulties and challenges. The latter part has been elaborated by about 300 words from about 60 words in the Central Economic Work Conference report.

Clear signal

The Government Work Report has sent a clear signal that China's development still faces more favorable conditions than adverse factors and that the basic trend of economic recovery has not changed. It is necessary to both boost confidence and adhere to bottom-line thinking. The country should be fully prepared to deal with various risks and challenges, make good use of favorable conditions, and fully mobilize all aspects.

Some voices have questioned China's economic growth rate last year, but viewed from the perspective of the long-term relationship between commonly used economic indicators and economic growth, this questioning is debatable.

For instance, from 2003 to 2023, the correlation between China's electricity generation and actual economic growth was 0.753, and for the United States, it was 0.687, which showed a stronger positive correlation between the two indicators in both China and the US.

Specifically, from 2021 to 2023, the correlation in China was highly positive at 0.997, while in the US, it was weak at 0.277. It indicates China's economic fluctuations in recent years, while such a correlation in the US suddenly disappeared.

Last year, China's electricity generation grew by 6.2 percent, an increase of 2.8 percentage points compared with the previous year, corresponding to an economic growth rate of 5.2 percent and an increase of 2.2 percentage points year-on-year.

Electricity generation in the US changed from a 3 percent increase in 2022 to a decrease of 1.2 percent last year. But it didn't correspond to an economic growth rate of 2.5 percent and an increase of 0.6 percentage point year-on-year.

A prosperous job market is believed to be an important manifestation of the resilience of the US economy. However, some analysts have pointed out that official US employment data are based on "income", while unemployment data are based on "per household", which may exaggerate the prosperity of the US job market.

If a person takes three part-time jobs, according to the "per household" standard, it counts as one person employed, but according to the "income" standard, it counts as three people employed.

Second, the projected deficit rate of China is not high, but the actual fiscal expenditure intensity is not weak either.

According to the Government Work Report, the country's deficit rate is projected at around 3 percent considering its comprehensive development needs and fiscal sustainability. The deficit scale is pegged at 4.06 trillion yuan ($565 billion), an increase of 180 billion yuan from last year's budget.

The 3 percent deficit rate is the same as last year's, lower than the market's previous expectation of around 3.5 percent. However, considering the following factors, the actual fiscal expenditure intensity is higher than last year's.

First, China plans to issue special long-term national bonds for several years. The plan is aimed at major tasks and the security of key areas. Second, the country plans to arrange 39 trillion yuan of special bonds for local governments, an increase of 100 billion yuan from last year.

Third, 1 trillion yuan of government bonds were issued in the fourth quarter of last year, and 500 billion yuan was carried over for use this year. It is expected that fiscal revenue will continue to recover and grow this year, and coupled with funds transferred in, the scale of general public budget expenditure will be 28.5 trillion yuan, an increase of 1.1 trillion yuan from last year.

Therefore, after the budget draft was disclosed at the two sessions, the market did not feel disappointed.

Optimized debt

This year's budget still sees an increase in the central government's deficit, while local governments maintain a deficit of 720 billion yuan for the third consecutive year. It reflects the vision of optimizing the structure of central and local government debts.

However, it is still unclear whether the issuance of special long-term national bonds will follow the approach of last year's increase in government bonds, all of which are transferred to local governments through transfer payments, and both the principal and interest are repaid by the central government.

Of course, if last year's approach is adopted, it is necessary to establish a government debt management mechanism compatible with high-quality development within the framework of the new round of fiscal and tax system reform, and make clear the fiscal and administrative powers of central and local governments.

Considering that the current recovery of consumption in China is still on track, with deep "scar effects" after the COVID-19 pandemic, it may also be important to increase public service consumption expenditures that are provided by government departments to society, as well as net expenditures on goods and services provided free of charge or at low prices to resident households.

Faced with the above challenges, three aspects are critical to improving social expectations.

The first is to launch better-than-expected macroeconomic measures to guide economic operations back to a reasonable range. In recent years, China has remained strategically focused on high-quality development and adhered to structural adjustment as the main focus and policy stimulus as a supplement to cope with downward economic pressure.

However, among the myriad measures, the ones that can stabilize the economy are the most practical and effective. Macroeconomic policies should be forward-looking, enrich the toolbox, and leave room for redundancy, to ensure that timely and effective measures can be introduced when needed.

This year's economic growth rate should not be lower than the compound average growth rate from 2020 to 2023. At the same time, economic growth should be accompanied by moderate price increases and improved employment for key sections of the population.

The second is to launch greater-than-expected risk-prevention policies to guide major risk factors toward convergence. Real estate, local government debt, and small and medium-sized financial institutions are the focus areas for China's current risk-prevention and control.

The country must adhere to both short- and long-term approaches and treat both the symptoms and root causes to ensure that systemic risks do not occur.

The third is to launch more reform and opening-up measures to reshape market confidence with landmark events. Deepening reform and opening-up is a necessary means to do away with institutional obstacles, stimulate the vitality of market entities and enhance the drivers of economic development. Substantive measures need to be implemented to reshape policy credibility.

To this end, it might be dealing properly with some market-focused events or resolving some important issues that are not that eye-catching, but are important bottlenecks for the market.

The writer is global chief economist at BOC International.

The views do not necessarily reflect those of China Daily.