Hong Kong offices a crown jewel for high-yield hunters

Updated: 2016-08-31 07:53

By Oswald Chan in Hong Kong(HK Edition)

|

|||||||

|

Cheung Kong Center (left) - the headquarters of tycoon Li Ka-shing's business empire - stands beside the Bank of China Tower in Central. According to US real estate advisory firm Colliers International, yields from investments in the office property sector in major Asia Pacific centers currently range from 3 to 6 percent. Jerome Favre / Bloomberg |

Talk of Li Ka-shing's property flagship unloading its stake in one of Hong Kong's prime commercial buildings at the upper end of the valuation scale, as well shrinking bond yields worldwide, have injected fresh zeal into the city's offices market.

Market experts say the local office property sector stands to benefit from prospects of higher investment returns as continued purchases of government bonds by central banks have further depressed global bond yields.

Li's Cheung Kong Property Holdings (CK Property) - the property flagship of CK Hutchison Holdings (CK Hutchison) - is reported to be contemplating disposing its 75-percent stake in The Center - a 73-story commercial skyscraper located in the Central business district - with a property valuation appraisal of between HK$26.6 billion and HK$50 billion.

If the property could go for up to HK$50 billion, it would be one of the highest prices ever fetched in the city's office investment market.

Another key factor driving investors in the local offices sector is compressed global bond yields, with continued asset purchase programs of buying government bonds by central banks having pushed bond yields to their lowest levels, thereby stimulating investment in properties.

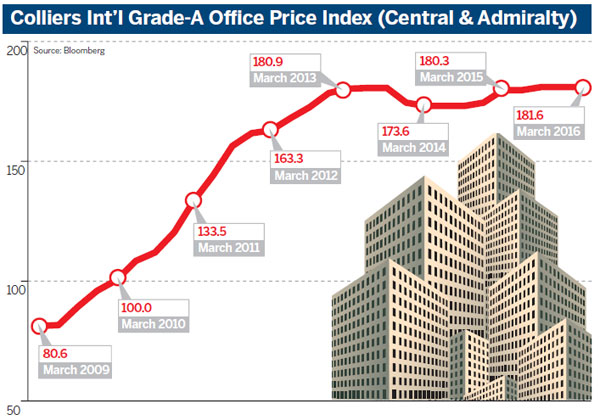

According to US real estate advisory firm Colliers International, yields from investments in the office property sector in major Asia Pacific centers currently range from 3 to 6 percent. The Australian and Japanese office markets offer a yield of 4 percent above government bonds, while the Hong Kong market can generate a return of 2 percent higher than holding government bonds.

Data from Jones Lang LaSalle show that Hong Kong developer First Group Holdings forked out HK$789 million for a commercial development site in Kwai Chung last month. The price was 12 percent over the higher end of market expectations and surpassed the record price set by Sun Hung Kai Properties for a nearby business development site in May.

Sources said First Group will spend HK$1.3 billion to build a new office building, which is expected to be completed in 2019.

Britain's shock move in June to quit the European Union has generated global macroeconomic uncertainty that has further dented global bond yields, forcing investors to switch from bonds to properties. Companies' urge to expand and landlords' investment portfolio rebalancing have added momentum to investing in Hong Kong's office sector.

Commercial property landlords' efforts to rebalance their property investment portfolios to achieve greater shareholder value have thus facilitated more office investment deals.

Li has been rebalancing his global investment portfolio in recent years by cashing his assets in Hong Kong and on the Chinese mainland, and redirecting the proceeds into utility and infrastructure assets in European countries.

His elder son, Victor Li Tzar-kuoi, who is deputy chairman and managing director of CK Property, told investment analysts earlier this month that the group can sell any commercial property it holds, except Cheung Kong Center and Hutchison House.

Besides Cheung Kong Center and Hutchison House, CK Property's office portfolio in the SAR includes China Building, The Center, the Harbourfront, Wayland House and 99 Cheung Fai Road.

Chinese mainland enterprises, on the other hand, are particularly eager to establish their footprints in Hong Kong, and have remained active in the local office investment market.

Last month, Shenzhen-based Cheung Kei Group acquired the East Tower of One HarbourGate in Hung Hom from local developer Wheelock & Co for HK$4.5 billion. The West Tower of One HarbourGate was snapped up by mainland insurer China Life Insurance (Overseas) for HK$5.85 billion in November last year.

Investment bank Daiwa Capital Markets believes that the market has underestimated the potential and strength of the local office sector.

"The Shenzhen-Hong Kong Stock Connect should provide a boost to the sector's prospects in so far that it's a step forward in the Chinese mainland's attempt to liberalize or reform its financial sector," said Jonas Kan Kwok-yu, head of Hong Kong and mainland property research at Daiwa Capital Markets.

"We see the Hong Kong office sector as the leading segment in the local property cycle since the second half of 2003, rather than one that has lagged behind the residential and retail sectors," said Kan. "The fundamentals of the office sector are stronger than they appear."

Colliers International reckons that Hong Kong's office sector has been the most resilient, with both institutions and private investors showing strong interest in this segment.

"The (Hong Kong) office sector would be ideal for some core funds or institutions to deploy their capital and having it locked for three to four years until the global financial situation becomes clearer," said Reeves Yan, capital markets and investment services senior director at Colliers International.

oswald@chinadailyhk.com

(HK Edition 08/31/2016 page9)