Interest rates and RRR may see cuts

China may need additional monetary easing measures such as cutting interest rates or the reserve requirement ratio soon to facilitate the upcoming issuance of special treasury bonds, experts said on Monday.

Other factors to be taken into consideration include lukewarm financing demand in April and persistent low price growth — situations that have attracted close attention from policymakers, they said.

"If interest rates or the RRR are not cut this week amid the weak inflationary environment, then (I think) interest rates will be cut in June. That is, a cut in interest rates is on its way, sooner or later," said Hong Hao, chief economist at GROW Investment Group. The RRR refers to the proportion of deposits that banks must keep in cash as a reserve.

The People's Bank of China, the country's central bank, is due to unveil the medium-term lending facility rate — the policy benchmark for interest rates — on Wednesday, after the Ministry of Finance released on Monday the issuance schedule of ultra-long-term special treasury bonds worth 1 trillion yuan ($138 billion).

The issuance schedule spans from this month to November and begins with the issuance of 30-year bonds on Friday. Bonds with 20-year and 50-year tenors will be offered from May 24 and June 14, respectively, the ministry said.

Hong said the ultra-long-term special treasury bond issuance represents a meaningful expansion in the fiscal deficit that the market is looking for, which will help rejuvenate the credit cycle and help achieve the annual economic growth objective of around 5 percent.

Shao Yu, a board member of the Shanghai Institution for Finance & Development, a think tank, said policy coordination from the PBOC is needed to ensure the efficacy of the bonds in bolstering the economy.

With the issuance of ultra-long-term government bonds to generate more demand for liquidity, the PBOC needs to take more easing measures to maintain low financing costs for the government bonds and the real economy, Shao said.

The PBOC said on Friday in its first-quarter monetary policy report that it will "strengthen policy coordination and cooperation to keep prices at an appropriate level", citing insufficient demand as the fundamental reason for current low price levels.

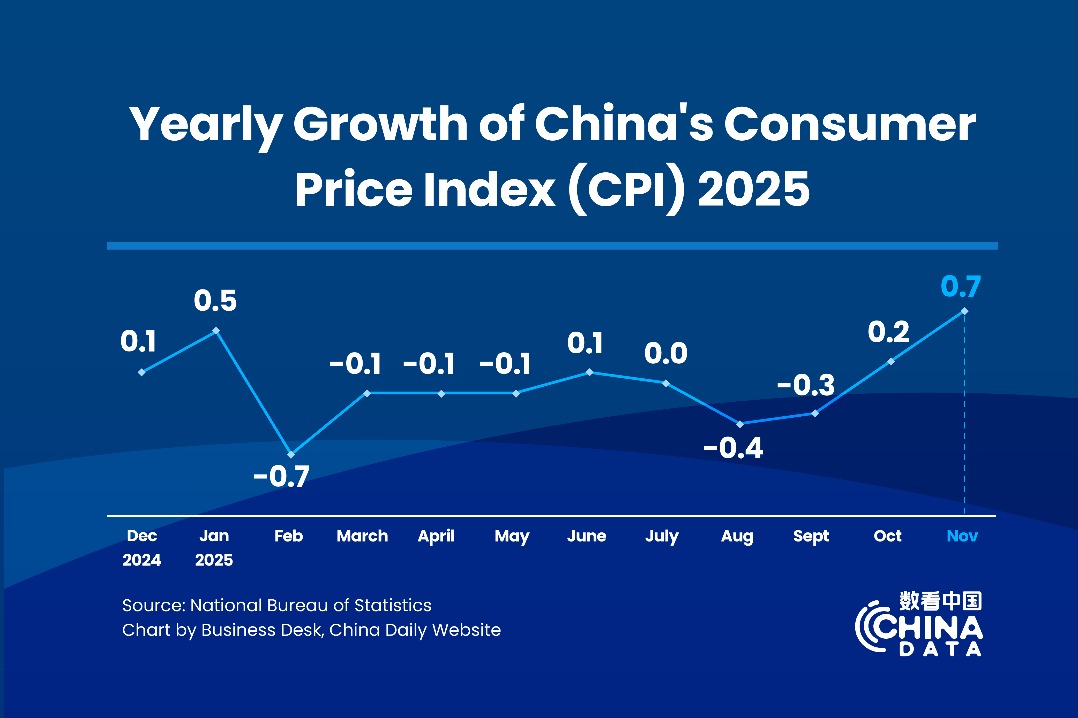

Official data showed the country's consumer price index, a key indicator of inflation, rose 0.3 percent year-on-year in April after a 0.1 percent gain in March.

Financial data also pointed to lackluster demand as the PBOC said on Saturday that the country's increment in aggregate social financing — the total amount of financing to the real economy — came in at 12.73 trillion yuan in the first four months, down $3.04 trillion yuan compared with the same period last year.

In April, the increment in aggregate social financing even turned negative, falling by 198.7 billion yuan, the first negative reading since October 2005, according to market watcher Wind Info.

Jacqueline Rong, chief China economist at BNP Paribas, said the PBOC is likely to implement additional 25-basis-point cuts in both the MLF rate and the RRR this year, which could take place as early as this month or in June.

Rong said that the PBOC often takes immediate action following meetings of the country's top leadership that call for easing funding costs, while the issuance of both treasury bonds and local government bonds is set to speed up and necessitates an accommodative monetary environment.

Liu Zhihua contributed to this story.