RMB market rides on cross-trading link

Updated: 2015-04-30 06:51

By Selena Li in Hong Kong(HK Edition)

|

|||||||

The Hong Kong-Shanghai Stock Connect program has provided bankers with new opportunities to create renminbi (RMB)-denominated products that can enhance the city's position as the premier offshore renminbi center.

A top Hong Kong financial official called the cross-trading link, which is expected to be extended to the Shenzhen bourse later this year, "a significant breakthrough in our (offshore) renminbi market development".

Speaking at a recent bankers' conference, Secretary for Financial Services and the Treasury Ceajer Chan Ka-keung said that since the early days of the offshore renminbi market development, bankers have been looking for "an investment asset that investors could actually buy using RMB".

The growing popularity of the stock connect program, launched in November, has set the direction for expanding the renminbi market.

Local bankers have been trying to enlarge the offshore renminbi pool as the city faces growing competition from newer centers, particularly Singapore, London and, more recently, Toronto. Their search has zeroed in on new investment products that can attract global investors keen on holding renminbi assets.

Bankers said equity Exchange-Traded Funds (ETFs) will be the next desirable renminbi product in the making for both onshore and offshore markets. The marketable security tracks an index, a commodity, bonds or a basket of assets.

"For domestic investors to diversify wealth to overseas assets, it would be interesting if ETFs are added to the (Shanghai and Hong Kong) stock connect program this year. That way, mainland domestic investors can have a wide choice of investments," said Ian Cohen, chief strategy officer global equities markets at HSBC.

Mark Austen, chief executive officer of the Asia Securities Industry and Financial Markets Association, told China Daily that apart from the existing renminbi-denominated bonds, bond ETFs are products with lower risk exposure to retail investors.

"If that company defaults on the bond, investors can lose close to everything. For retail investors, ETFs are the preferred instruments to invest in," he said.

Regulators and exchanges are being comfortable with ETFs because the capital flow in those instruments can be better monitored, alleviating concerns about hidden capital outflow, Cohen added.

Currently, the issuance of renminbi-denominated bonds remains a major measurement of the size of an offshore market.

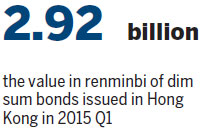

Dim sum bonds (bonds denominated in renminbi) issued in Hong Kong this year totaled 2.92 billion yuan ($471.2 billion) as at the end of March, compared to Singapore's 2.74 billion yuan, according to Reuters data.

Issuance in Hong Kong took a dive at the beginning of the year due to tightened liquidity. But the market dynamics have changed since April when the removal of restrictions triggered a rush by mainland fund-management companies to snap up Hong Kong stocks.

Financial experts have called for a bigger increase in the quota for the Qualified Foreign Institutional Investor (QFII) program, or even removal of the daily quota for two-way flow under the stock connect program.

Increasing QFII quotas would attract more foreign investors, and the resulting increase in capital flow can fuel the further development of renminbi products in the offshore market, bankers said.

Another promising development involves discussions to allow a wider scope of renminbi assets to be transferred to the offshore market, helping to open up the asset-backed securities (ABS) market to foreign investors, said Carmen Ling, managing director and global head of renminbi solutions at Standard Chartered in Hong Kong.

The issuance of ABS products, a type of security backed by a pool of assets, including consumer loans, leases or receivables other than real estate, is projected to be worth up to 3 trillion yuan by 2018.

selena@chinadailyhk.com

(HK Edition 04/30/2015 page9)