| .contact us |.about us | |

|

|

|||||||

|

||

| Advertisement | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Huge potential of China's corporate bond market ( 2003-07-25 10:26) (China Daily HK Edition)

Corporate bond market in the coming years is enormous, but there are still problems to be tackled, according to a senior executive in the securities industry.

Since the country first embarked on its policy of opening up in the late 1970s, China's stock and governmental bond sectors have developed rapidly. Corporate bonds, however, the third major fund-raising tool in the capital market, lag far behind stocks and government bonds, said Li Wei, general manager of the Fixed Income Department of China Securities Co Ltd. China Securities is one of the largest securities companies in the Chinese mainland and was the main underwriter of State treasury bonds last year, registering record sales of 5.9 billion yuan (US$713.4 million). Li's viewpoint is echoed by other industry insiders. Dr Ba Shusong, an expert on the securities industry, said in a recent article that compared with other countries, China's corporate bond market potential is huge.

In the United States, the market value of bonds, including corporate bonds, is equivalent to 143 per cent of the country's gross domestic product (GDP). In Japan, the figure is 96 per cent, while in the 15 member nations of the European Union, the figure is 82 per cent. On a global scale, the average market value of bonds is about 95 per cent of the world's GDP. However, the market value of bonds in China, including corporate bonds, makes up only about 29 per cent of GDP, Ba said. Of the overall number of bonds in China, the outstanding value of State treasury bonds equals about 1,700 billion yuan (US$205.56 billion) and the outstanding value of financial bonds comes to about 1,000 billion yuan (US$120.91 billion), while the outstanding value of corporate bonds is only 40 billion yuan (US$4.83 billion). Furthermore, the Chinese bond market is lacking in derivatives, Dr Ba said. The very fact that the country's corporate bond market is so small indicates that there is ample room for further development. In addition, as the capital market develops, both the internal and external environments for corporate bond issuers will steadily improve. Li said there were many reason to be optimistic about the future of the nation's corporate bond market. ** First of all, the Chinese government is paying more and more attention to the importance of corporate bonds in the capital market, he said. Development of the corporate bond market was also included in China's 10th Five-Year Plan (2001-05). In his government report delivered to the National People's Congress last year, former Premier Zhu Rongji pledged to accelerate development of the corporate bond market so as to increase the ratio of direct fund-raising in the market. At present, the governmental departments concerned and related sectors of society are joining together to prepare for the launch of the country's corporate bond market, with the main purpose being to narrow the gap between that market and the already flourishing stocks and governmental bonds markets. "The issuance of corporate bonds by listed companies and the eventual establishment of our country's corporate bond market will be major steps towards a mature domestic corporate bond market," Li said. ** The second favourable sign, Li continued, is that the corporate bond market has been expanding since 2000. This year, the quota of corporate bond issuance is likely to hit 100 billion yuan (US$12.09 billion).

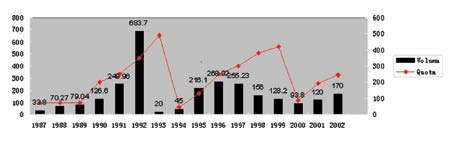

At the same time, the issuance size of a single corporate bond has also increased, now usually exceeding 1 billion yuan (US$120.9 million), he said. China Mobile, one example, issued 5 billion yuan (US$604.5 million) worth of corporate bonds in the market in 2001, but last year the figure shot up to 8 billion yuan (US$967.3 million). ** Third, the right to issue corporate bonds has been extended to local enterprises, while in the past almost all issuers active in the Chinese capital market were mega-sized State-owned enterprises directly under the control of the central government. For instance, said Li, of the 10 enterprises which received special approval to issue corporate bonds from the State Council last year, six were local firms. This year, some local businesses working on projects with plans to issue bonds of less than 1 billion yuan (US$120.9 million) have also won support from the central government. Of the first batch of corporate bonds to be issued, the value of bonds contributed by local enterprises accounts for 28.57 per cent of a planned total of 7 billion yuan (US$846.4 million). "Such changes indicate that more enterprises will be able to enter the corporate bond market and that the corporate bond market has begun moving towards diversification," Li said. ** Fourth, controls governing fund usage have been eased to some extent, with some enterprises adopting the non-project fund-raising method. In these cases, companies raise money from corporate bond issues to repay their bank loans instead of directly investing the money into project construction. China Mobile has done so, using most of the funds it raised from corporate bond issuance to pay back loans owed to a banking consortium. "Although the usage of funds raised from corporate bond issuance is still related to construction projects, this marks a major step towards market-orientation and the adoption of international norms," Li said. ** Fifth, the process of issuing corporate bonds is gradually becoming more streamlined. One obvious trend is that the method of issuance is shifting to a paper-less procedure. In China, the registration of corporate bond custody as well as the trading and settlement systems have basically been established, laying the foundation for more technologically sophisticated online issuance and underwriting processes. "Online issuance and underwriting are now in the testing stage. This will greatly reduce the cost of corporate bond issuance and also create the basis for market integration and custodianship in the future," Li said. In addition, interest rates for corporate bonds are increasingly being determined by market forces, and institutional investors now play a dominant role in the corporate bond investment sector. ** Sixth, the liquidity of corporate bonds is on the rise thanks to the joint efforts of the government and industry players, Li said. By the end of this June, a total of 34 corporate bonds (excluding convertible corporate bonds) had been traded on the Shanghai and Shenzhen stock exchanges. At present, a total of 20 corporate bonds are being traded on the two stock exchanges with a combined market value of 44.6 billion yuan (US$5.39 billion).

Statistics indicate that between 1998 and 2002, the total traded volume of corporate bonds on the Shanghai Stock Exchange recorded an average annual growth rate of 125 per cent. Between January and June of this year, the volume of corporate bonds traded on the Shanghai Stock Exchange reached 14.266 billion yuan (US$1.725 billion), representing an increase 2.33 times that for the same period last year. Along with the growing liquidity of corporate bonds, the difference in earnings ratios between corporate bonds and the market has narrowed, a factor that will come to influence interest rates in the primary market more and more, Li said. ** Finally, Li believes that reform is starting to have an impact on risk control mechanisms for corporate bonds. Before 2001, the majority of corporate bond issuers adopted the "guarantee by related enterprises" style of risk control. Recently, however, some issuers have opted for bank guarantees. As a kind of commercial guarantee, a bank guarantee can effectively enhance the credit ratings of issuers and increase the certainty of repayment, an important leap forward in the successful development of the country's corporate bond market. Still, despite the encouraging prospects, Li stressed there remain problems that must be dealt with to accelerate the development of the corporate bond market. He called for simplifying the examination and approval procedures currently weighing down the corporate bond sector. Among the other pressing issues demanding attention, streamlining the legal requirements with which corporate bond issuers must comply, enhancing the functions and capabilities of intermediaries, fostering investor risk awareness and liberalizing interest rates all need to be adequately addressed in order to ensure a sound and healthy corporate bond market, he said.

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| .contact us |.about us | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Copyright By chinadaily.com.cn. All rights reserved |